How Smart Travelers Save Hundreds Overseas UsingMulti-Currency Accounts |

Discover how smart travelers save hundreds overseas using multi-currency accounts, better exchange rates, and low-fee international spending strategies. |

|

There is a moment many travellers recognise, often only after it has already cost them money. You arrive in a new country, still adjusting to the pace of the journey, and you check your bank balance or make your first withdrawal. At first, it looks harmless. A small fee here, a conversion charge there, a slightly worse exchange rate than expected.

Nothing dramatic on its own.

Yet by the end of the trip, the total quietly adds up to hundreds. Most people never fully track it. They simply accept it as part of travelling abroad. But increasingly, a different group of travellers has started to challenge that assumption and change the way money moves across borders entirely.

The slow shift away from traditional travel money

For a long time, travel cash cards and bank debit cards were considered sufficient. They worked well enough for holidays and short trips. You could load money, spend overseas, and move on without much thought. However, the financial system behind those tools has not kept pace with how people travel today.

Traditional banks still rely on older international payment systems that introduce multiple layers of cost. These are often not presented as a single visible fee.

Instead, they appear in different places, such as foreign transaction charges, ATM withdrawal fees, conversion margins, and dynamic currency conversion at the point of sale.

Individually, they seem small. Together, they create a consistent drain on travel budgets.

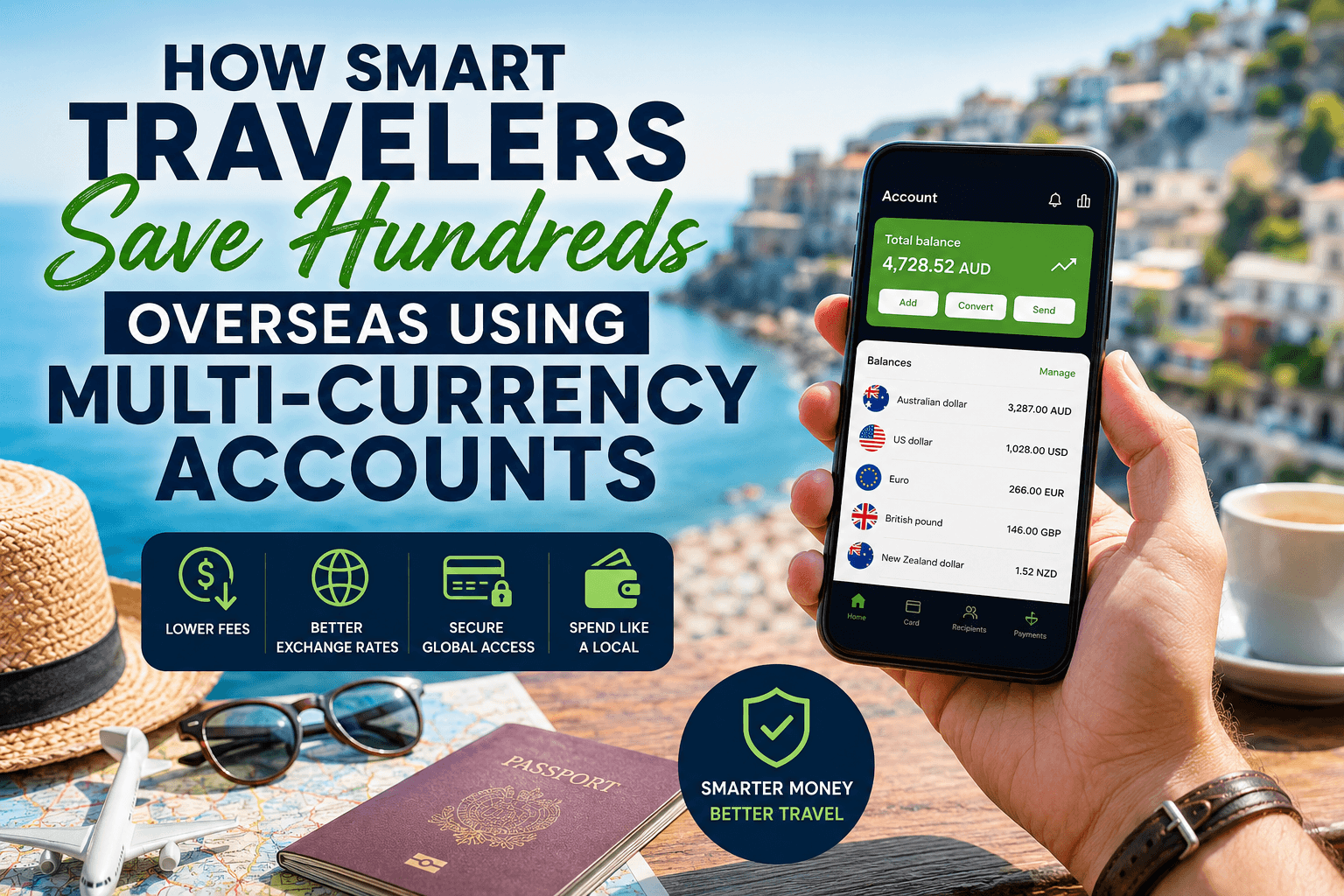

What a multi-currency account actually does

A multi-currency account changes how money behaves when you are outside your home country. Rather than forcing every transaction through a single domestic currency, it allows you to hold and use multiple currencies in a single account.

This means you can hold Australian dollars, US dollars, euros, pounds, yen and others depending on the provider, and use them directly when you travel.

The key difference is control. Instead of every payment being converted automatically in the background, you decide when conversion happens and how your money is held.

This simple shift reduces unnecessary conversion events, which is where most hidden costs occur.

Where travellers actually lose money without realising it!

The most expensive parts of travel spending are rarely obvious. One of the main issues is the exchange rate margin applied by traditional banks. While travellers often assume they are getting the real exchange rate, banks typically add a margin that is not clearly highlighted.

Over time, this creates a meaningful difference in total spend. Another common issue is airport and kiosk currency exchange services. These are designed for convenience and urgency, not value.

The exchange rate offered is usually significantly worse than market rates. A further problem is dynamic currency conversion. This occurs when a payment terminal offers to charge you in your home currency instead of the local currency.

It feels helpful, but it often locks in a poorer exchange rate and adds hidden costs.

How multi-currency accounts reduce travel costs

The savings from multi-currency accounts do not come from a single dramatic discount. They come from removing repeated small inefficiencies across every stage of travel spending.

One of the most important benefits is access to exchange rates that are much closer to the mid market rate. This is the rate you typically see when you search for currency conversion online, before bank markups are applied.

Another benefit is the ability to spend directly in local currency. This avoids forced conversions at checkout and reduces exposure to dynamic currency conversion traps.

ATM withdrawals can also become more cost efficient depending on the provider, particularly when compared to traditional bank debit cards that layer multiple fees on top of each withdrawal.

Why the mindset of smart travellers is different

Experienced travellers tend to think differently about money overseas. Rather than viewing fees as unavoidable, they see them as a system to be managed.

This creates a subtle but important shift in behaviour. Instead of focusing only on getting cheaper flights or hotels, they also focus on how efficiently money moves during the trip itself.

This mindset often leads to better financial outcomes without requiring any change in lifestyle or travel experience.

Multi-currency accounts versus travel cash cardsTravel cash cards were designed for a different era of travel. They are typically prepaid, require manual loading, and often come with reload fees, inactivity charges, and less flexible currency handling.

Multi-currency accounts operate more like modern financial platforms. They are app based, allow real time currency management, and are designed for ongoing international use rather than one off trips.

For people who travel frequently or live across multiple countries, this difference becomes significant.

Why this matters more now than ever

Travel is no longer limited to short holidays. Many people now move between countries for extended periods, work remotely, or manage international income streams.

In this context, traditional banking tools start to feel restrictive. Multi-currency accounts are increasingly used not just for travel, but as everyday financial infrastructure for global living.

The emotional impact of financial clarity while travellingBeyond the numbers, there is a psychological benefit that many travellers do not anticipate.

When you are no longer worried about hidden fees or unexpected charges, the experience of travelling feels lighter. You are less likely to second guess small purchases or constantly calculate conversion costs in your head.

That reduction in mental friction makes travel feel more relaxed and more present.

Frequently asked questions:

Do multi-currency accounts really save money?

Yes, in many cases, they reduce hidden fees and improve exchange rates compared to traditional banks, particularly for frequent international spending.

Can you withdraw cash overseas?

Most multi-currency accounts support international ATM withdrawals, although fees and limits vary depending on the provider.

Are they better than bank cards?

For regular travellers, they often are. Traditional bank cards can include foreign transaction fees and less competitive exchange rates. Do you need to convert money before travellingNot always. Many users convert as needed or hold multiple currencies in advance, depending on travel plans.

Are they safe to use overseas?

Most modern platforms include security features such as instant card freezing, transaction alerts, and multi-factor authentication.

|